A. Inflation expectations

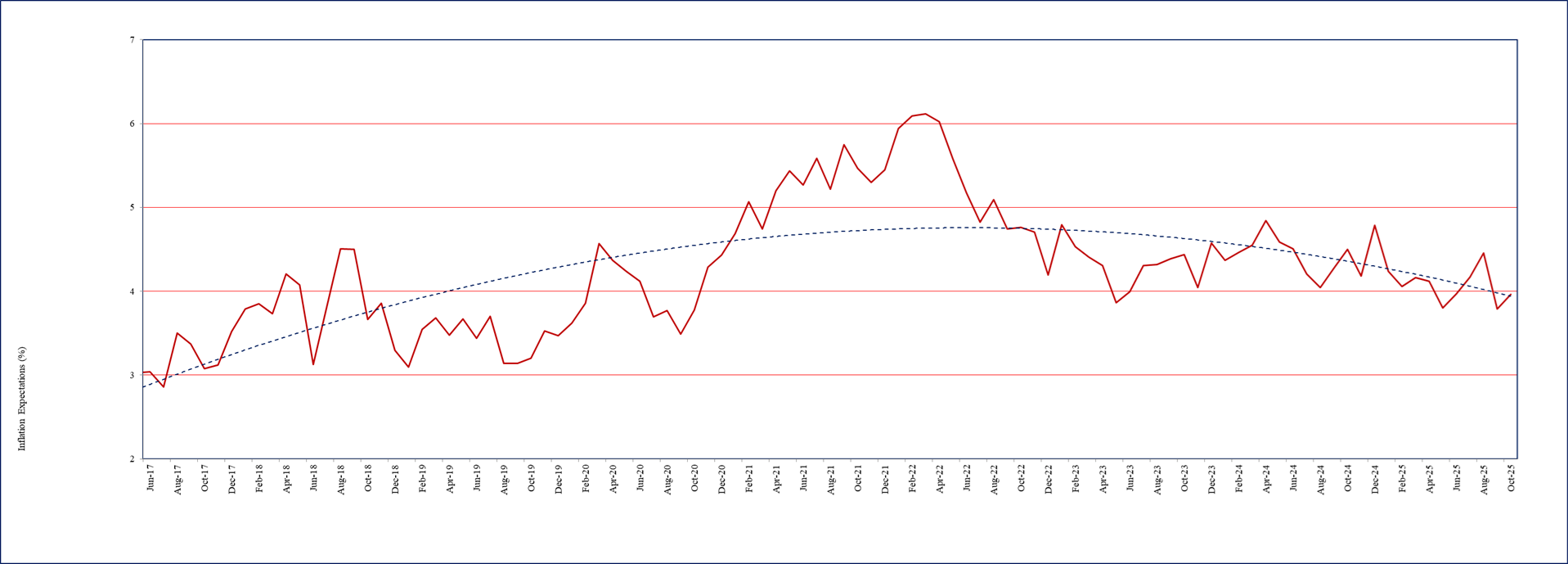

- One year ahead business inflation expectation, as estimated from the mean of individual probability distribution of unit cost increase, has increased by 18 basis points to 3.97% in October 2025 from 3.79% reported in September 2025. Firms’ average inflation expectation during the past 12 months has remained anchored around 4.14%. The trajectory of one year ahead business inflation expectations is presented in Chart 1.

- The uncertainty of business inflation expectations in October 2025, as captured by the square root of the average variance of the individual probability distribution of unit cost increase, has remained the same around 1.90% as reported in September 2025.

Chart 1: One year ahead business inflation expectations (%)

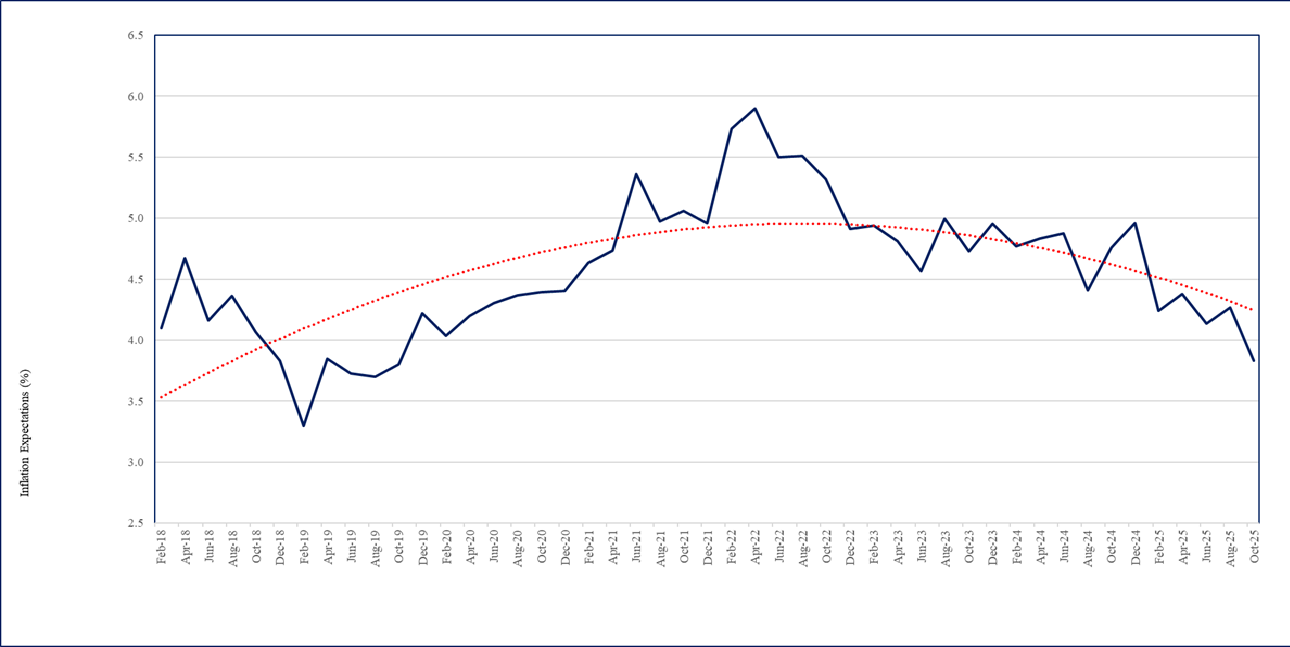

- Respondents were also asked to project one year ahead CPI headline inflation through an additional question using a probability distribution. This question is repeated every alternate month, coinciding with the month of RBI’s bi-monthly monetary policy announcement.

1The Business Inflation Expectations Survey (BIES) provides ways to examine the amount of slack in the economy by polling a panel of business leaders about their inflation expectations in the short and medium term. This monthly survey asks questions about year-ahead cost expectations and the factors influencing price changes, such as profit, sales levels, etc. The survey is unique in that it goes straight to businesses - the price setters - rather than to consumers or households, to understand their expectations of the price level changes. One major advantage of BIES is that one can get a probabilistic assessment of inflation expectations and thus get a measure of uncertainty. It also provides an indirect assessment of overall demand condition of the economy. Results of this Survey are, therefore, useful in understanding the inflation expectations of businesses and complement other macro data required for policy making. With this objective, the BIES is conducted monthly at the Misra Centre for Financial Markets and Economy, IIMA. A copy of the questionnaire is annexed.

Companies are selected primarily from the manufacturing sector. Starting in May 2017, the “BIES – October 2025” is the 102 nd round of the Survey. These results are based on the responses of around 900 companies.

- The businesses in October 2025 expect one year ahead CPI headline inflation to be 3.83%, significantly down by 44 basis points from 4.27% reported in August 2025 (Chart 2). Firms’ uncertainty of CPI inflation expectations has declined to 0.87% from 0.95% reported in August 2025.

Chart 2: Expected CPI headline inflation (%) - one year ahead

B. Costs

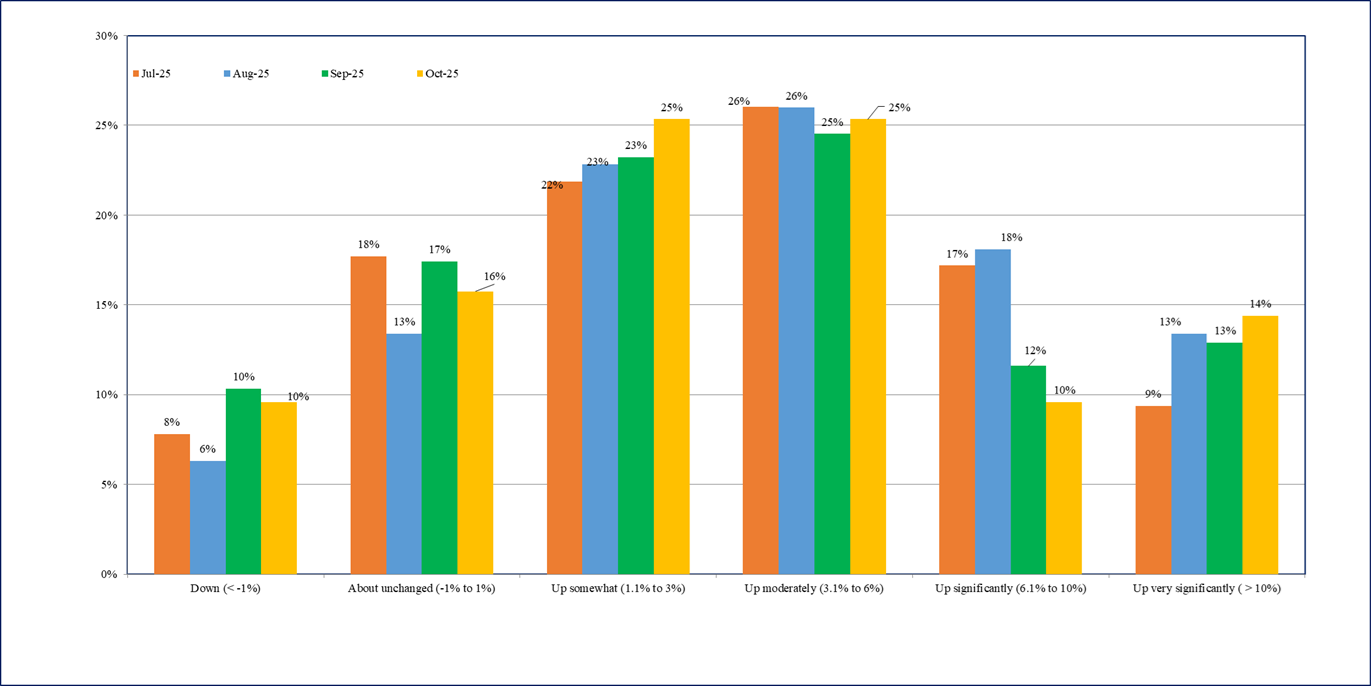

- Overall, the cost perceptions data in October 2025 does not signal increase in cost pressures.

- The percentage of firms perceiving significant or very significant cost increase (above 6%) has declined marginally to 24% from 25% reported in September 2025 survey (Chart 3).

Chart 3: How do current costs per unit compare with this time last year? – % responses

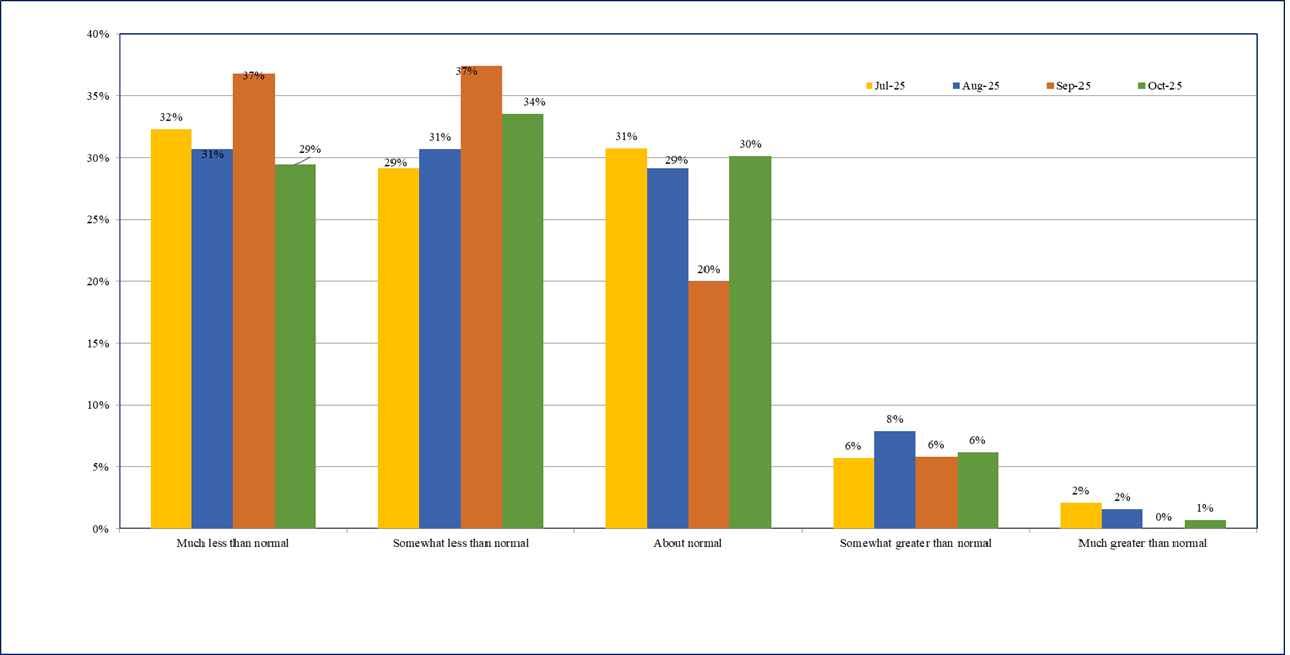

C. Sales Levels

- During June-October 2025, over 60% of the firms reported ‘much less than normal’ or ‘somewhat less than normal’ sales 2 (Chart 4).

- The percentage of firms reporting ‘about normal’ or more sales during September-October 2025 has remained the same around 38%.

Chart 4: Profit Margins - % response

D. Profit Margins

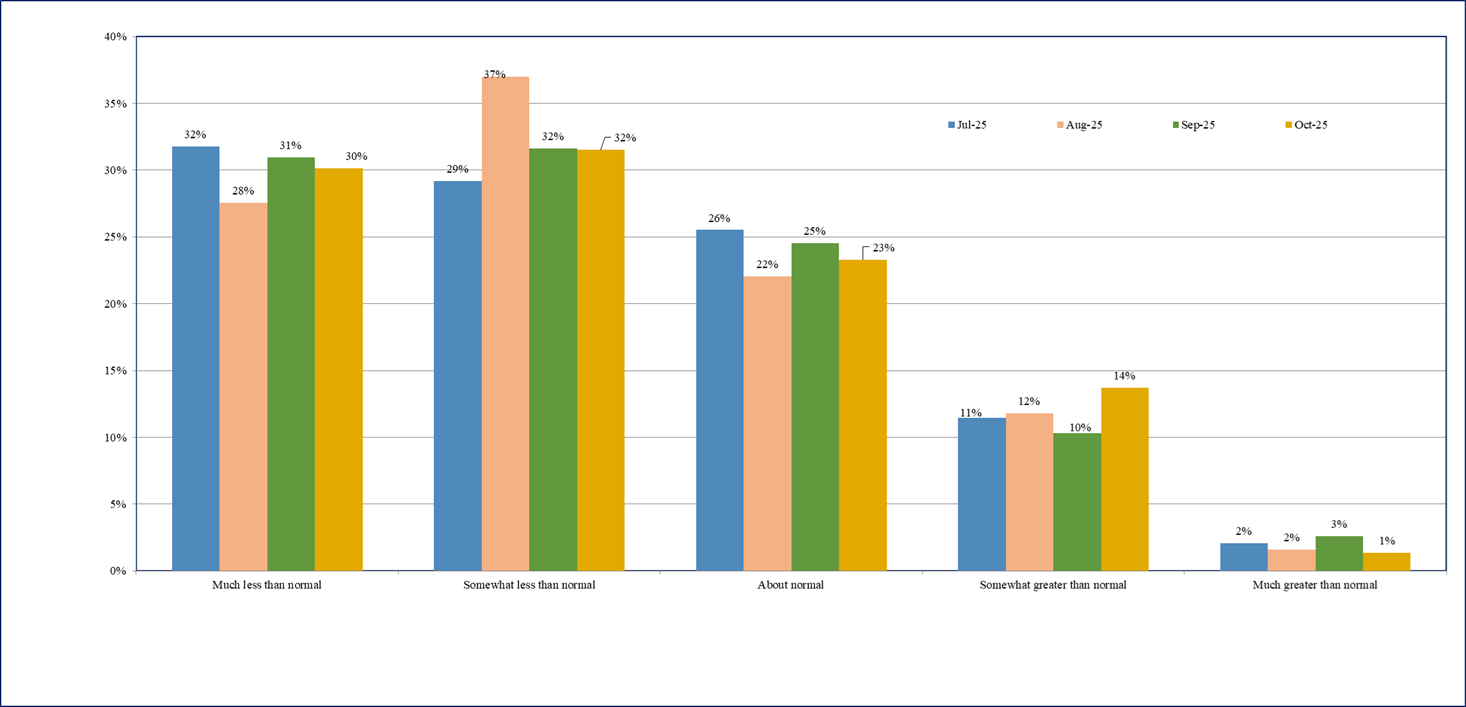

- The percentage of firms reporting ‘about normal’ or higher profit expectations in October 2025 has sharply increased to 37% from 26% reported in September 2025 (Chart 5).

- Profit margin expectations improved due to decline in cost pressures.

Chart 5: Profit Margins - % response

2Normal means as compared to the average level obtained in the preceding 3 years, excluding the Covid-19 period.

Business Inflation Expectation Survey (BIES) – Questionnaire

|

A. Current Business Conditions

Q1. How do your current PROFIT MARGINS@ compare with "normal" * times?

o Much less than normal

o Somewhat less than normal

o About normal

o Somewhat greater than normal

o Much greater than normal

Q2. How do your current sales levels compare with SALES LEVELS@ during what you consider to be "normal"* times?

o Much less than normal

o Somewhat less than normal

o About normal

o somewhat greater than normal

o Much greater than normal

@ of the main or most important product in terms of sales.

*"normal" means the average level obtained during the corresponding time point of preceding 3 years, excluding the Covid-19 period.

|

B. Current Costs Per Unit^

Q3. Looking back, how do your current COSTS PER UNIT compare with this time last year?

o Down (< -1%)

o About unchanged (-1% to 1%)

o Up somewhat (1.1% to 3%)

o Up moderately (3.1% to 6%)

o Up significantly (6.1% to 10%)

o Up very significantly (> 10%)

' of the main or most important product in terms of sales. |

|

C. Forward Looking Costs Per Unit$

Q4. Projecting ahead, to the best of your ability, please assign a percent likelihood (probability) to the following changes to costs per unit$ over the next 12 months.

o Unit costs down (less than -1%)

o Unit costs about unchanged (-1% to 1%)

o Unit costs up somewhat (1.1% to 3%)

o Unit costs up moderately (3.1% to 6%)

o Unit costs up significantly (6.1% to 10%)

o Unit costs up very significantly (> 10%)

$ of the main or most important product in terms of sales.

Values should add up to 100%.

|